Embedded Insurance Is Moving Fast: How to Launch Without Rebuilding Everything

Notes from Insurance Innovators Nordics, Copenhagen - March 2026

Earlier this month, our CEO Emmanuel Cheret took the stage at Insurance Innovators Nordics in Copenhagen to address a question that comes up in nearly every conversation we have with established insurers: how do you launch embedded insurance at the pace the market now demands, without first running a multi-year core transformation programme?

The Nordic markets continue to be a useful reference point for these discussions - embedded models, digital-first distribution, and customer-centric design are further along here than in most of Europe. The audience reflected that: insurers, brokers, MGAs, and ecosystem players all working on the same set of problems from different angles.

Below is a distilled version of the argument, with the slides we used to support it.

The opportunity is real, and the gap is widening

The market numbers around embedded insurance are by now well-rehearsed: a $700Bn opportunity by 2030, according to Deloitte, BCG, and KPMG estimates. What's more telling is who is currently moving fastest to capture it.Cover Genius is now serving 30M customers and grew 107% last year. Neat raised a $50M Series A on the back of 2,000+ partnerships and reached profitability in two years. Wrisk has secured a $12M Series B working with OEMs like BMW, Volvo, and Stellantis. Zego crossed a $1bn valuation with 17M policies in a category they essentially defined.

Meanwhile, most established insurers - the players with the brand, the balance sheet, and the local distribution that should make embedded insurance a natural extension - remain in the back seat. The question isn't whether incumbents are lagging. It's why.

The accepted explanation doesn't match what we observe

The standard answers are familiar. "Core transformation is needed first." "They're too big to innovate." "Risk-averse culture, lack of courage." We hear these framings constantly, and they've become the default explanation for slow movement on embedded insurance. The argument we made in Copenhagen is that this diagnosis is incomplete - and the prescription it leads to is the actual problem.Core transformation programmes typically run 18 to 36 months.

They carry significant execution risk. And critically, the ROI case for new business - embedded distribution, affinity partnerships, digital-first product lines - is rarely clear within those programmes. Core modernisation is justified, designed, and prioritised around existing volume. New distribution models get squeezed into the backlog and frequently deprioritised when trade-offs need to be made.The result is predictable: insurers that wait for core transformation to "finish" before launching embedded products end up watching the market form without them.

This isn't an argument against core modernisation. It's an argument against treating it as a prerequisite for entering embedded insurance.

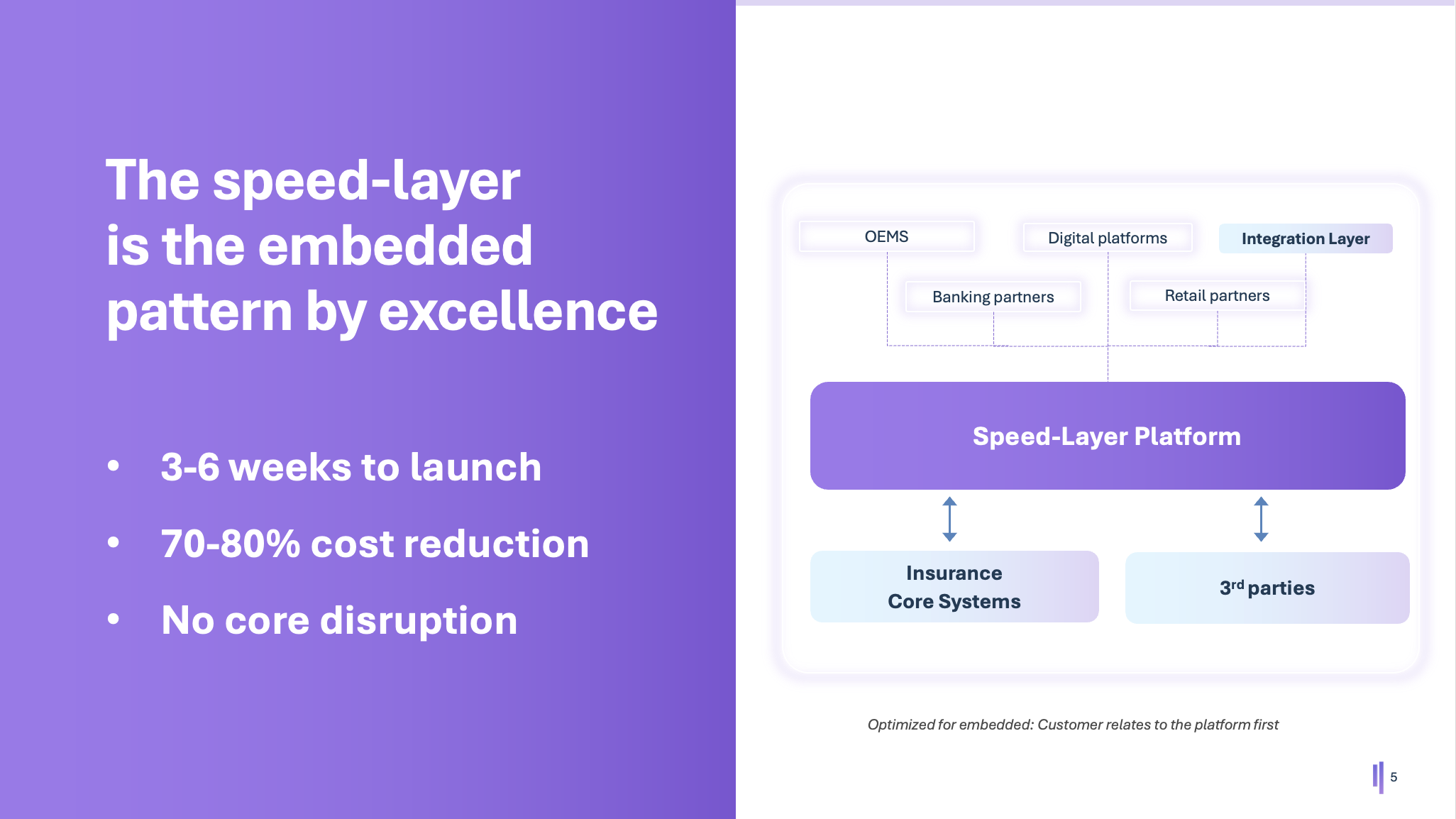

The speed-layer pattern

There is a different architectural choice available, and it's the one we see working in practice: a speed-layer platform running alongside existing core systems, optimised specifically for embedded distribution.

The speed layer sits between the insurer's core and the distribution edge - OEMs, banking partners, digital platforms, retail partners. It handles what core systems aren't built for: rapid product configuration, partner-specific integration, modern APIs, and the customer-first experience that embedded distribution requires. The core remains the system of record where it needs to be. The speed layer takes on everything that needs to move at partner speed rather than IT release-cycle speed.

The speed-layer is the embedded insurance pattern by excellence.

In practical terms: 3 to 6 weeks to launch a new product or partnership, 70-80% lower cost than building inside the core, and no disruption to existing operations. These aren't theoretical numbers - they're what we and our clients are consistently delivering on the platform.

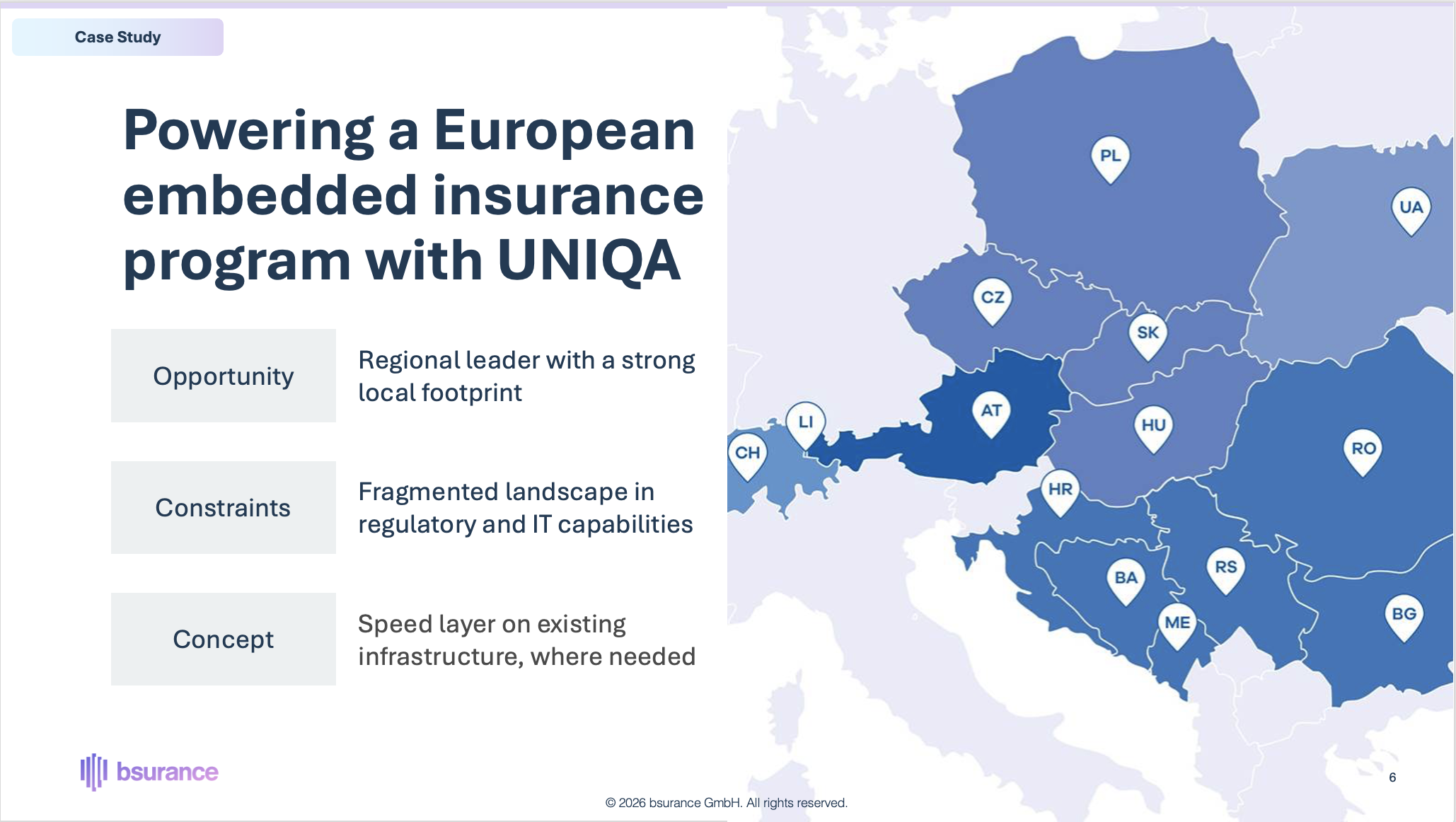

What this looks like in practice: the UNIQA programme

The most concrete reference point we shared in Copenhagen is our work with UNIQA.UNIQA is a regional leader across Central and Eastern Europe with strong local presence in markets ranging from Austria and Czechia to Croatia, Romania, Bulgaria, and beyond.

The opportunity for embedded insurance in their footprint is significant. The constraint is also significant: a fragmented landscape of regulatory frameworks, IT capabilities, and local operational realities across more than a dozen countries.The approach has been to deploy the speed layer where needed, on top of existing infrastructure, country by country - not to harmonise everything first and then launch, but to launch where the opportunity is sharpest and let the platform absorb the variation.A few learnings from this work that we shared on stage:

On the success-factor side: Speed to market that traditional approaches simply can't match. No disruption to the core business. Distribution partners, once they see what's possible, want more of it. And - perhaps most underrated - internal adoption: when business teams realise what they can do without IT dependency, new product ideas start surfacing organically.

On the critical-learnings side: Embedded insurance is genuinely new territory for most established players, and guidance is essential - the technology alone isn't enough. And modern systems represent a real rupture from how teams have worked for years; showing, not telling, is what shifts mindsets.

Powering a European embedded insurance program at scale with UNIQA

Implications by player type

The question we got most often after the talk was: "What does this mean for us specifically?" The answer depends on where you sit.

For insurers: Partner now. The window to take a leading role in embedded insurance is open but not indefinite. Launch in weeks rather than months, give your distribution partners better APIs than your competitors offer, and do it without disrupting your core programme.

For brokers: Your edge is access. You have the partnerships, the risk expertise, and the speed advantage. What you typically lack is platform infrastructure - and that's now available without building it yourself.

For MGAs: Don't rebuild. The combination of product expertise and distribution access is your strength. Building proprietary platform infrastructure dilutes that focus and increases risk. Build at the edge, partner for the core platform, launch faster.

Closing thought

The conversation in Copenhagen reinforced something we've been observing across markets: the embedded insurance opportunity is no longer being debated. The question has shifted from whether to how - and within how, the dominant question is how to move fast without breaking what already works.The dual-speed approach isn't a compromise. With the right architecture, it delivers material gains on speed, cost, and risk simultaneously. And it removes the false choice between "transform the core first" and "miss the window."For insurers, brokers, and MGAs working on these questions in 2026, there has rarely been a better moment to build.

Thanks to the Insurance Innovators team for hosting an excellent event, and to the audience in Copenhagen for the questions and conversations that followed. If you're working on embedded insurance and would like to compare notes, we'd be glad to connect.